Smart Ways to Build a Moat Around Your Wealth

Have you taken steps to protect the assets you have worked so hard to build?

Chances are, you know someone who has been sued. Maybe that someone is you.

The fact is, your enviable position as a successful person comes with a major downside: You’re a potential magnet for lawsuits—which may very well be frivolous and unfounded—and other attacks that can wreak havoc on your financial health.

That means you need to take steps to protect the assets you’ve worked so hard to build. Otherwise, you may jeopardize the financial security of yourself and your family.

Why you need asset protection

The logic of asset protection planning is clear: You build a moat around your assets that is as difficult as legally possible for litigators, creditors and others to cross. Instead of trying to fight it out with you in court for months or years and risk losing, the litigant sees that the only reasonable option from a legal standpoint is to settle for pennies on the dollar—or, ideally, to leave empty-handed.

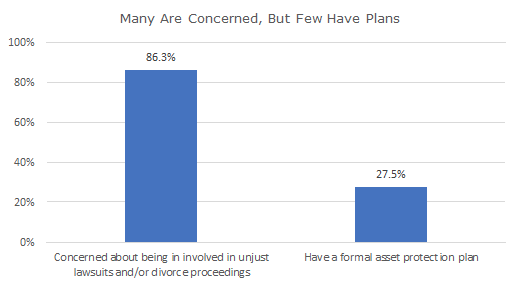

You probably recognize the threats to your wealth from others. According to research, more than 86 percent of successful business owners say they are concerned about becoming the object of unjust lawsuits or being victimized in divorce proceedings.

Here’s the bad news: Only about a quarter (27.5 percent) of successful business owners have a formal asset protection plan in place. Whether you are a business owner or not, with the risk you face in our litigious culture, this number is likely far too low.

Five key steps to protect assets

If you’re one of the many successful people who lack an asset protection plan—or you’re curious whether your existing plan is up to snuff—consider these key steps.

1. Get protected before a claim against you is made. You can do a lot to protect your wealth before a liability arises—but thanks to a concept known as “fraudulent conveyance,” very little after. As with insurance, the time to have asset protection in place is well before you need it—or even think you might need it.

2. Cover the basics. Evaluate your liabilities and other related insurances and maximize them as best you can. The fastest, easiest—and cheapest—move you can make is to take out a large umbrella policy to safeguard assets. Another simple but powerful strategy is to place your assets in someone else’s name, such as your spouse’s (assuming you have a great deal of trust in your spouse and your marriage). If you’re sued, those spouse-controlled assets are often untouchable.

3. Consider advanced asset protection strategies. The ultra-wealthy often take sophisticated steps to protect their wealth once they have covered the basics. Options to consider include:

- Equity stripping. Some ultra-wealthy business owners protect their assets from unjust and frivolous lawsuits by using bank loans to strip out the equity in their businesses. Conceptually, it’s simple. You take out a loan from a bank and secure the loan with the assets (such as equipment or real estate). This way, the bank has preference over judgments obtained by creditors. For creditors to get to the encumbered assets, they would first have to pay off the bank loan.

- Captive insurance companies. A captive insurance company is a closely held insurance company set up to insure the risks of the parent company. The owner of the parent company wholly owns the captive insurance company. Therefore, the business owner controls the operations of the captive insurance company (including underwriting, claims decisions and the investment policy).

- Onshore and offshore trusts. Currently, a number of states allow for domestic asset protection trusts, while countries such as the Bahamas, Belize, the Cook Islands and Nevis (among others) are good locations for offshore trusts. Assets placed in these are generally out of reach of creditors. That said, the rules governing these trusts vary greatly depending on the jurisdiction. Understanding the specifics of the jurisdiction is therefore critical.

4. Be sure your attorney or other professionals are qualified to help you protect your assets. Far too many financial professionals are not in a position to provide guidance on and implementation of many asset protection solutions. Take equity stripping, for example. Our research has found that fewer than 10 percent of financial advisors or the specialists they work with are familiar with equity stripping and that less than 1 percent have ever provided it to a client.

5. Avoid big mistakes that will trip up your asset protection efforts. Many of these more advanced asset protection strategies are complex and require a deep familiarity with and understanding of how they work to set up and execute them effectively. If poorly structured, asset protection strategies will have no “teeth” when they’re needed most—and your assets may not be nearly as safe as you assume.

ACKNOWLEDGEMENT: This article was published by the BSW Inner Circle, a global financial concierge group working with affluent individuals and families and is distributed with its permission. Copyright 2017 by AES Nation, LLC.

Investment advisory services offered only by duly registered individuals through AE Wealth Management, LLC (AEWM). AEWM and Carolina Retirement Planners, LLC are not affiliated companies. Investing involves risk, including the potential loss of principal. Any references to protection benefits and lifetime income generally refer to fixed insurance products, never securities or investment products. Insurance and annuity product guarantees are backed by the financial strength and claims-paying ability of the issuing insurance company.

AW11175157